Flow Analysis

BTC held 56k support for most of last week, and was having a look at 60k resistance during early Asia trading on Friday morning, when news of the new COVID strain hit the wires. Bond yields collapsed hard, and eventually BTC followed in the London morning, trading down to 54k within about 12 hours. Since then we have tried and failed a few times to break that level. However this morning the market rallied hard on the perception that Omicron is not particularly lethal, testing 58k briefly, despite the fact that we would need to wait a few more days for a better understanding of the new strain’s vaccine resistance. ETH has again traded very well throughout the price drop on Friday, dropping 10.5% high to low, while BTC dropped 9.5%. Since market highs on 10th November, BTC has dropped 16.5% and ETH has dropped only 11%.

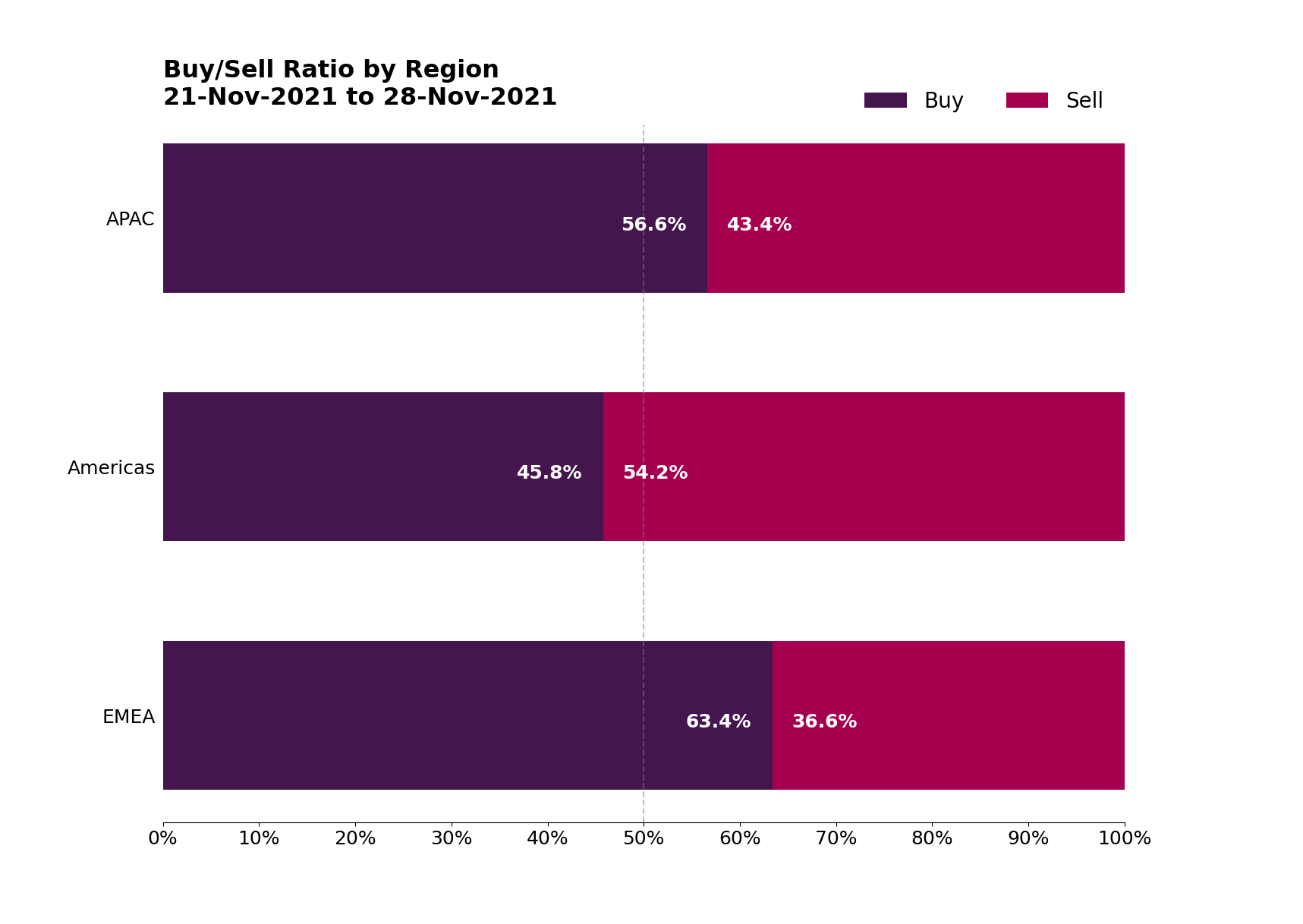

Our flows have still been biased to the long side in the majors, though for the first time in a few weeks, we have seen better buying in BTC (55.0% buying) than in ETH (52.3% buying). Elsewhere we have seen strong buying in XRP, and strong selling in DOT. Regionally, the Americas have provided the stronger sell flows (54.2% selling), with EMEA (63.4% buying) and APAC (56.6% buying) providing the bid side. In terms of client category, the primary buying has been done by crypto exchanges (67.8% buyers) and banks (65.0% buying).

In the crypto rates world, annualised 1-month futures basis tightened by around 5% on Friday with the spot selloff, to around 6.5%. This led to funding arbitrage funds taking profit by unwinding their short basis positions, causing a small intraday bounce off the c.5% lows. Whilst abrupt tightening of this nature isn't uncommon, Friday’s move brought the basis across the whole term structure to its lowest since September. However, the weekend saw it make up half of this drop. Strong ETH borrow demand faded over the past week, replaced by BTC demand.

In options land, the price action from Friday has not really had much impact, which suggests to us that vols are priced for the sort of moves we saw in May this year, and therefore may be liable to further underperformance. The crypto market felt quite balanced already last week with Friday’s selloff in price remaining orderly, and vols not jumping for any protracted period of time. Put that all together, and it indicates that vols are just too high, especially if we stay away from the topside. And indeed, the options desk is seeing mainly vol sellers at the moment.

Dec BTC ATM implied vols is at 77%, which is at the low end of the recent range for 1 month volatility (77-87%). Yet with realised volatility struggling to get above 70% for the past couple of months, we can see a risk of vols getting a bit of a shoeing if spot settles into a range for a while. It’s also worth mentioning that the mid-curve March BTC 25 delta skew is now slightly favouring puts, quite unusual for a 4-month contract. In ETH, the March 15k strike is still dominant: now a 10 delta call, it is currently trading 136 vols, down marginally from last week, but not as much as Dec ATM (97 vol down 6 on week) and Mar ATM (113 vol down 7 on week). As a result, Mar 25 delta skew is still 6 vols for calls, whereas Dec skew is 8 vols for puts: make of that what you will.

Overall Friday was a messy end to a holiday-impacted week. With a bit of luck, Omicron will turn out to be a highly contagious variant which doesn't make people very sick. However, if that script doesn't play out, we could be in for a long unhappy northern hemisphere winter, with more supply side issues feeding into a rather non-transient looking inflation picture. It might just be that these sorts of risk-off events are buying opportunities for inflation hedges like BTC.

B2C2 is the crypto-native liquidity provider across market conditions. 450+ institutions globally, including agency OTC desks, aggregators, banks, exchanges, FX brokers and hedge funds, rely on B2C2’s full service offering for 24/7 access to the crypto market.

Since it was founded in 2015, B2C2 built its technology, products and services to meet the evolving needs of diverse institutions. Continuously innovative, B2C2 is trusted by clients to find solutions to industry challenges, such as creating the first crypto ISDA Master Agreement in 2018.

Acquired by Japanese financial group SBI in 2020, B2C2 remains a standalone company, headquartered in the UK, with offices in the US and Japan. B2C2 OTC Ltd. is authorised and regulated by the UK’s Financial Conduct Authority (FRN 810834). For more information, please visit https://www.b2c2.com

Sign up to our news alerts to receive our regular newsletter and insights into the crypto market direct to your inbox.